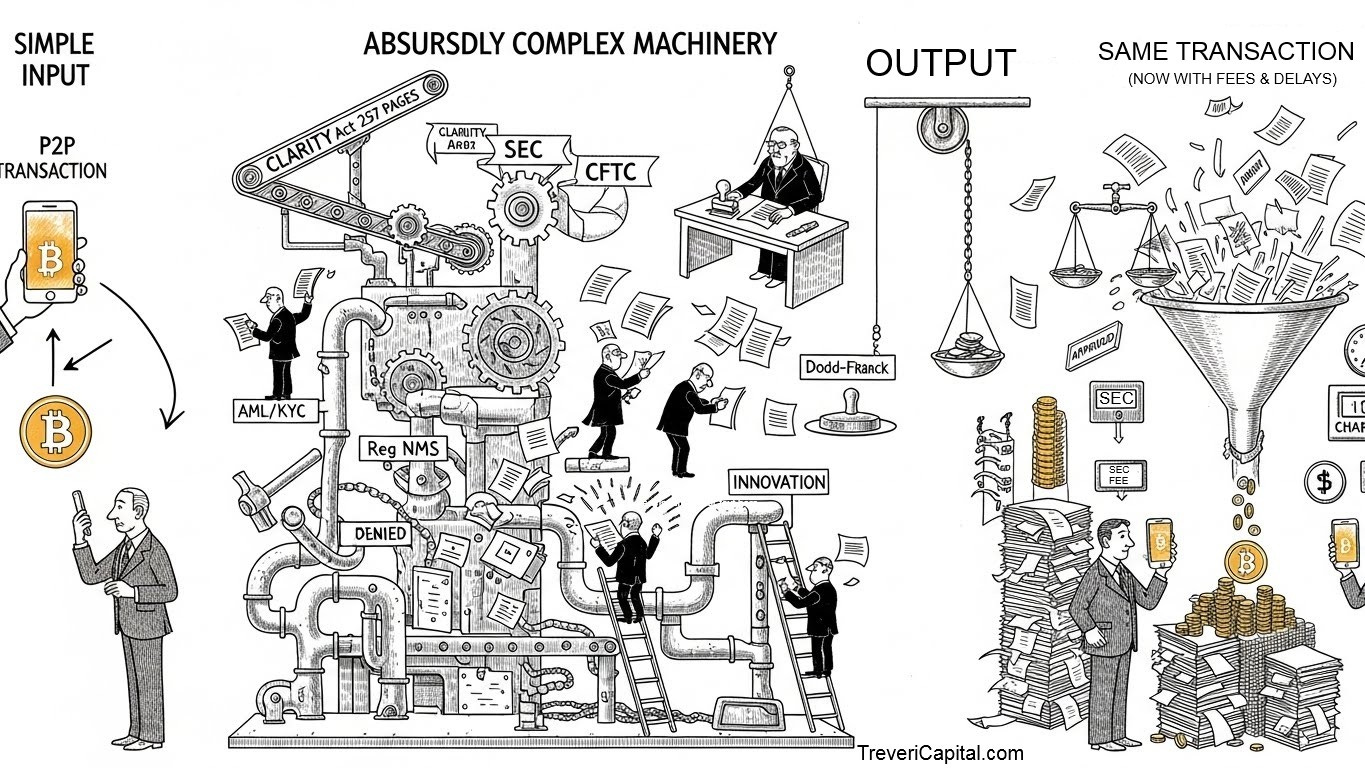

The CLARITY Act: Another Regulatory Disaster in the Making

Why Congress’s attempt to regulate crypto will fail - just like Dodd-Frank and Reg NMS before it

The Pattern: Good Intentions, Terrible Outcomes

Exhibit A: Dodd-Frank (2010)

The Promise: Prevent another 2008 financial crisis, protect consumers, eliminate “too big to fail.”

The Reality:

Made the biggest banks bigger through consolidation

Killed community banks under compliance burden

Pushed companies to delay IPOs by 10-20 years[1]

Created a two-tiered financial system: sophisticated investors access private growth, retail investors get table scraps

Didn’t prevent a single risk - just made them more opaque

Exhibit B: Regulation NMS (2005)

The Promise: Create a “National Market System” with best execution and fair access.[2]

The Reality:

Fragmented markets across dozens of venues

Spawned high-frequency trading arms race

Created dark pools that hide institutional order flow

Made markets so complex that even professionals can’t explain them

Led to flash crashes and market instability

The Punchline: The SEC is now working on “Reg NMS 2.0” to fix the problems created by Reg NMS 1.0. Twenty years later, still not finished.[3]

Exhibit C: Regulation ATS

Tried to regulate Alternative Trading Systems. Result? Pushed trading into even darker corners, created regulatory arbitrage, and made institutional trading less transparent than before.

The CLARITY Act: Same Script, Different Market

Now Congress wants to “clarify” crypto regulation with a 257-page monstrosity[4] that will:

1. Kill U.S. Innovation The world’s crypto developers and builders will do what every smart entrepreneur does: go where they’re welcome. Dubai, Singapore, Switzerland, and Hong Kong are rolling out the red carpet while we roll out red tape.[5][6][7]

Result: The next generation of financial infrastructure gets built elsewhere. U.S. loses tax revenue, job creation, and strategic advantage.

2. Create Regulatory Capture Notice who supports this bill? Incumbent exchanges who can afford the compliance costs. Notice who’s hurt? Every startup, small competitor, and innovative project that can’t staff a compliance department.

Coinbase even withdrew support when they realized the Senate version benefits traditional banks at crypto’s expense.[8] When the most compliant crypto company in America says a bill is “worse than nothing,” that should tell you something.

3. Increase Costs, Reduce Access Every compliance requirement gets passed to customers as:[9]

Higher trading fees

Custody fees that didn’t exist before

Minimum account sizes that exclude smaller investors

Geographic restrictions

The people hurt most? Retail investors and small businesses - the exact people politicians claim to protect.

4. Solve Problems That Don’t Exist FTX collapsed because of fraud - already illegal. Do Kwon (Terra/Luna) - arrested under existing laws.[10] Sam Bankman-Fried - 25 years in prison under wire fraud statutes.[11]

We don’t need new regulations. We need to enforce the laws we have.

The Real Problem: Regulators Don’t Understand What They’re Regulating

The CLARITY Act treats all “digital commodities” the same, when Bitcoin, Ethereum, and other networks have completely different architectures, risk profiles, and use cases.[9] It’s like regulating “the internet” without understanding the difference between email, social media, and e-commerce.

The bill attempts to:

Regulate decentralized protocols as if they were centralized companies

Force disclosure requirements on software that has no disclosing entity

Require registration of activities that are, by design, permissionless

Apply securities frameworks to assets that aren’t securities

It’s a category error at the fundamental level. Legal experts have warned about the potential for regulatory arbitrage, where issuers could exploit definitional loopholes to recharacterize securities as commodities.[12] State securities regulators have also voiced concerns that the bill weakens their enforcement authority.[13]

The Better Path: Less Regulation, Not More

What actually works:

Prosecute fraud aggressively under existing criminal statutes

Let market forces work - bad actors get exposed and fail (see FTX)

Keep barriers to entry low so competition drives quality

Focus on disclosure rather than permission - let investors make informed choices

Protect property rights - clarify that individuals can custody their own assets

Bitcoin was created specifically to be censorship-resistant and permissionless. Trying to regulate it like a centralized financial instrument misses the entire point.

The Unintended Consequences (Coming Soon)

If the CLARITY Act passes, we’ll see:

10 years from now: “Reg CLARITY 2.0” attempting to fix the problems created by CLARITY 1.0

Brain drain: Top crypto engineers and entrepreneurs building outside the U.S.

Two-tiered access: Wealthy investors access crypto through offshore structures; retail investors locked into expensive, restricted U.S. platforms

Innovation elsewhere: The blockchain equivalent of Alibaba, Tencent, and TSMC - built in countries that welcomed the technology while we regulated it to death

National security risk: If crypto becomes systemically important (it will), the U.S. voluntarily gave up the home-field advantage

The Real Opportunity: When Everyone Else is Paralyzed

The best opportunities come when everyone else is frozen by uncertainty.

Right now, we are watching investors make the same two mistakes we saw in 2008, and again in 2020:

Mistake #1: Waiting for the “all clear” signal

They think once the CLARITY Act passes (or fails), then they’ll know what to do. But here’s what actually happens: By the time regulatory uncertainty resolves, Bitcoin is already 3x higher and they’ve missed the move. Clarity doesn’t create opportunity - it eliminates it.

Mistake #2: Confusing news with analysis

Every CLARITY Act headline triggers a reaction. “Should I buy? Should I sell? What does this mean?” That’s not investing - that’s emotional whiplash. The question isn’t whether the bill passes. The question is: Do you have 2-5% exposure to a non-correlated asset with a 10+ year time horizon? If yes, headlines don’t matter.

You don’t need to predict what Congress does. You need position sizing that lets you hold through any outcome. That’s the difference between trading noise and building wealth.

The psychology working against most investors:

Bad news always sounds smarter than good news. “CLARITY Act will destroy crypto” gets clicks. “Bitcoin ETFs now hold $100B in institutional assets” sounds boring. But pessimism has a terrible investment track record.

People also confuse “optimal” with “reasonable.” Sure, self-custody might be optimal for crypto purists. But Bitcoin ETFs are reasonable - no lost keys, no exchange risk, simple estate planning. In 20 years of watching people lose money, I’ve learned: Survival beats optimization.

Your advantage right now:

While everyone else debates what Congress might do, disciplined investors are:

Sizing positions they can hold through volatility

Using proven ETF structures instead of chasing complexity

Thinking in decades while others react to daily news

Building allocation strategies, not placing bets

The investors who build real wealth over the next decade won’t be the ones who perfectly timed regulatory news. They’ll be the ones who acted with discipline while everyone else waited for certainty that never came.

Smart Investors Prepare While Politicians Posture

Markets self-regulate through competition, reputation, and the consequences of failure. Heavy-handed regulation doesn’t prevent harm - it just concentrates power in fewer hands, raises costs for everyone, and pushes innovation to more hospitable jurisdictions.

The gold rush doesn’t come to the place with the most rules. It goes to the place with the clearest property rights and the least interference.

The bill passed the House on July 17, 2025 with a vote of 294-134.[14] Congress should kill this bill and let the market work.

What This Means for Your Portfolio

Here’s the good news: You don’t need to navigate this regulatory mess to gain Bitcoin exposure. SEC-approved Bitcoin ETFs provide institutional-grade access through your existing brokerage account - no exchanges, no custody headaches, no regulatory gray zones.

While the CLARITY Act creates chaos for crypto exchanges, Bitcoin ETFs offer:

Traditional custody at many US broker dealers such as Interactive Brokers our favorite custodian.

Simple estate planning (transfers like any other security)

Clean tax reporting (standard 1099 forms)

Fiduciary clarity for RIAs

The question isn’t whether to allocate to Bitcoin - it’s how to do it intelligently within a diversified portfolio using proven ETF structures, not speculative crypto platforms.

I work with high-net-worth individuals and advisors on Bitcoin ETF allocation strategy: optimal position sizing, portfolio construction, risk management, and fiduciary compliance. No proprietary products. No custody. Just independent advice on accessing Bitcoin exposure through institutional vehicles.

Ready to discuss your portfolio? Contact us now!

sources:

[1] Dodd-Frank’s Impact on IPO Market

Multiple academic studies document increased compliance costs delaying public offerings from average 5-7 years pre-Dodd-Frank to 10-15+ years post-2010. See: Michael Ewens & Joan Farre-Mensa, “The Evolution of the IPO,” Annual Review of Financial Economics (2020)

[2] Regulation NMS (2005)

Securities and Exchange Commission

17 CFR 242.600-242.612

https://www.sec.gov/rules-regulations/regulation-nms

[3] SEC Proposing Reg NMS 2.0

“Order Competition Rule” proposed December 2022, still under consideration as of 2026

https://www.sec.gov/news/press-release/2022-225

[4] H.R. 3633 - Digital Asset Market Clarity Act of 2025

U.S. Congress, 119th Congress (2025-2026)

https://www.congress.gov/bill/119th-congress/house-bill/3633

[5] Dubai’s VARA Regulatory Framework

Virtual Assets Regulatory Authority

Clear licensing framework launched 2022

https://vara.ae/

[6] Singapore MAS Crypto Guidelines

Monetary Authority of Singapore

Payment Services Act framework

https://www.mas.gov.sg/

[7] Switzerland’s “Crypto Valley” Zug

Swiss Financial Market Supervisory Authority (FINMA)

Crypto-friendly framework established since 2017

[8] Coinbase CEO Withdraws Support for CLARITY Act

Brian Armstrong statement, January 14, 2026

“Coinbase CEO Brian Armstrong Rejects Senate Draft,” CCN.com, January 14, 2026

https://www.ccn.com/news/crypto/coinbase-ceo-armstrong-walks-away-supporting-clarity-act-why/

[9] CLARITY Act Analysis - Congressional Research Service

“Crypto Legislation: An Overview of H.R. 3633, the CLARITY Act”

Library of Congress, CRS Insight IN12583

https://www.congress.gov/crs-product/IN12583

[10] Do Kwon Arrest

Arrested March 2023 in Montenegro under existing securities fraud laws

Pending extradition to U.S. or South Korea

[11] Sam Bankman-Fried Conviction

U.S. v. Bankman-Fried, 25-year sentence (2024)

Wire fraud, conspiracy, money laundering - all existing statutes

U.S. Department of Justice

[12] Arnold & Porter Analysis: “CLARITY Act Concerns”

“Clarifying the CLARITY Act: What To Know About the House Crypto Market Structure Bill”

Legal analysis citing regulatory arbitrage concerns, September 2025

https://www.arnoldporter.com/en/perspectives/advisories/2025/08/clarifying-the-clarity-act

[13] NASAA Opposition Letter

North American Securities Administrators Association

Letter expressing concerns about weakening state authority, January 13, 2026

https://www.nasaa.org/wp-content/uploads/2026/01/NASAA-Expresses-Concerns-Regarding-the-Digital-Asset-Market-Clarity-Act-1.13.26-F.pdf

[14] House Vote on CLARITY Act (July 17, 2025)

Passed 294-134 with 78 Democratic votes

House Clerk Roll Call Vote #199

https://clerk.house.gov/Votes/2025199

[15] Senate Banking Committee - Response to Criticism

“Myth vs. Fact: The CLARITY Act”

Senator Tim Scott’s office, January 2026

https://www.banking.senate.gov/newsroom/majority/myth-vs-fact-the-clarity-act

Copyright © 2026 All rights reserved. This blog is copyright protected. No part may be reproduced, altered, or copied in any form without written consent. Information contained herein is for informational purposes only and should not be construed as an offer, solicitation, or recommendation to buy or sell securities, or personalized investment, tax or legal advice. The information has been obtained from sources believed to be reliable; however no guarantee is made or implied with respect to its accuracy, timeliness, or completeness. Authors may own the stocks they discuss. The information and content are subject to change without notice. Treveri Capital LLC is a California registered investment advisor. CRPC®, Chartered Retirement Planning CounselorSM are trademarks or registered service marks of the College for Financial Planning in the United States and/or other countries.